For those of you who aren’t into biking, and maybe even for those of you who are, it’s time now for another case study. This time we have a friend whom I’ll call Mike. Mike wants to know whether his pension portfolio is messed up or OK. Let’s take a peek and see what help we can provide, and what lessons we can also learn!

For those of you who aren’t into biking, and maybe even for those of you who are, it’s time now for another case study. This time we have a friend whom I’ll call Mike. Mike wants to know whether his pension portfolio is messed up or OK. Let’s take a peek and see what help we can provide, and what lessons we can also learn!

Mike knows I’m good with money, so he came to me with some questions. Obviously I told him, like I’m telling you right now, that I am not licenced to provide professional financial advice, and that this is for information purposes only. You should make your own decisions after seeking professional advice, or at least after doing enough research to know how to DIY your investments.

Mike’s employer provides him with a “Deferred Profit Share Plan” (DPSP). This is basically a pension where the company contributes some cash each year, and then Mike decides what investments to buy within his portfolio. Mike can neither add to nor withdraw from the plan as long as he’s with the company. Also, his choices are restricted to those set up by the company and the contracted fund provider.

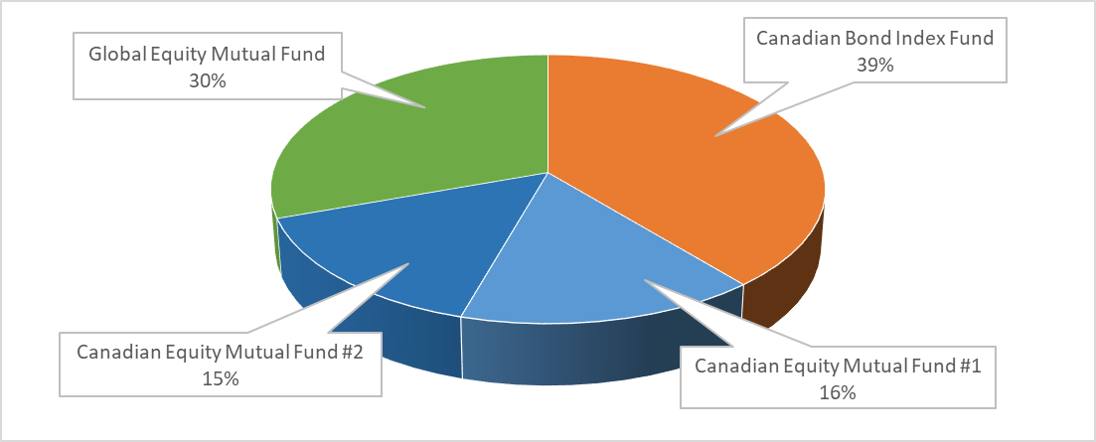

We started in person with some guidance on the basics and how to learn more. Then he shared where his DPSP account stands:

Here was my response, with some minor edits:

Initial Thoughts

Hi Mike,

Thanks for sharing your portfolio. Here are my initial thoughts. As always, let me know if you’d like to sit down together and go through this in more detail.

- I am not a financial advisor, so take everything I say with a grain of salt. 🙂

- I see opportunities to improve what you have, but at the same time I do not see any “oh that is BAD – fix it NOW” things.

- Your asset allocation* is very common and not unreasonable: about 60% equities, 40% income (bonds). Of the equities, you are about 50% Canadian and 50% US+International (to know the split on the latter, you will need to look into the fund details).

- Your equities are invested in active mutual funds, not passive index funds; this means that you are probably overpaying for fees by a meaningful amount (to know exactly, you’ll have to look into the fund details and compare to the fees of the comparable index funds); however your bonds are in a passive index fund.

- For info on choosing active vs. passive funds, check out www.canadiancouchpotato.com. In a nutshell, the theory goes that active funds cannot beat the market over any meaningful period of time, but charge high fees. Passive funds track the market, minus low fees. Therefore, in general over the long term, passive funds will outperform active funds after fees have been accounted for. I invest only in passive funds.

Next Steps

Here is my non-professional, personal recommendation on what you should do next. I am always available to help you work through it, if you like.

Here is my non-professional, personal recommendation on what you should do next. I am always available to help you work through it, if you like.

- Read up on passive vs. active investing at www.canadiancouchpotato.com; their “model portfolios” tab is a good resource. Then determine whether you prefer the passive approach or the active approach. Your DPSP fund provider offers both options.

- Determine your ideal asset allocation*. Just because you’re 60/40 equity/bond and then 50/50 Canadian/Non-Canadian does not necessarily mean that you should be there. To figure this out, you’ll need to know your time horizon (how long until you need the $$) and your risk tolerance (how much $$ you are prepared to lose). There are many online surveys that can help you with this. In fact, I would suggest starting on your fund provider’s account page; they probably have some tools there to help. Caution: MOST people think they have a higher risk tolerance than they actually do, which results in them panicking when stocks crash. Not good.

- Decide if you want to pick your own asset allocation or let your fund provider do it for you. They have the option of putting you into a bunch of active funds and then automatically adjusting your time horizon as you age. I personally don’t do this because I change my asset allocation myself. See previous point on passive “couch potato” investing. It’s easy, if you want to learn.

- Be sure that you understand “rebalancing” (buying/selling funds to bring you back to your ideal asset allocation.) The fund provider has an option to do this automatically for you for free.

- Asset allocation

- Equities

- Fixed income / bonds

- Active funds vs. passive funds (mutual funds vs. index funds)

- Time horizon

- Risk tolerance

- Rebalancing

Caution: MOST people think they have a higher risk tolerance than they actually do, which results in them panicking when stocks crash. Not good.

Additional Reading

* Here’s a summary of some key terms to know. I’ll let Google explain them to you, or I can in person if you prefer:

* Here’s a summary of some key terms to know. I’ll let Google explain them to you, or I can in person if you prefer:

Hope this helps! Let me know if you’d like to chat more about your portfolio. It might seem overwhelming at first, but it’s really quite simple once you start working on it.

Your Turn Now!

Your Turn Now!

Your Turn Now!

Your Turn Now!What do you think about Mike’s setup and choices? Any particular pieces of advice or links you’d like to share with him?

I hve two comments:

(1) if this was 2008 the mix of Canadian and us/international would be good. Right now he’s missing a good opportunity. The us economy is doing 4%+ growth while Canada is stagnating.

(2) a really important question is also who are the beneficiaries of the fund if something happens to him. A lot of people provide a direction for their spouse to receive the funds if they die, but don’t consider the possibility of their spouse predeceasing them. They should make sure that their spouse is the primary beneficiary if they die but that their kids are secondary if their spouses predeceases. A designation would almost surely save several thousand dollars in taxes and legal fees which can be easily avoided.

Good points. With #1, be careful not to fall into a “timing the market” philosophy. That growth ratio between the geographic areas could change any time. With #2, I fully agree.

I think “timing the market” is not doable in a micro sense unless you are a very sophisticated day trader, but I see very little wrong at looking at the macro trends and planning accordingly (with sufficient hedging).

I predicted that interest rates would stay low until a republican was in the whitehouse again in 2010. Low and behold, it stayed mostly sub 3% from 2010 until now, when it is creeping above 4% for some borrowers, and is generally on an upward trend. Correctly analyzing that a weak US economy resulting from bad policy choices was going to keep interest rates low was not much of a gamble.

Similarly, looking at the US performance over the last year, the DOW (which I’m going to use as a predictor of overall market performance, stood at roughly 13000 in late October 2012. From then until late October 2016 it grew to 18000 points. A difference of 5000 points over 4 years, or 17% over 4 years, for annual growth of 4.25%. From October 2016 to October 2017 it grew from 18000 points to 24000 points, a 25% increase in just one and a half years. Some of that is distorted by the new tax rules which really helped businesses in 2017, but that kind of difference is so significant it should be noted.

Compare that to Canadian performance: In October 2012 it was at 12,400. It grew from that to 14,500 in October 2016, a growth of about 15%, or 3.75%. Since then it has grown to 16,300 today, a growth of 12%, over a year and a half. Now, the US is pulling us up quite a bit, that much is evident from recent growth even in Canada, but our growth is less than half that of US performance over the same period.

Incidentally, noting that the trend of events happening in October in the US (namely presidential elections) have market effects, Canada similarly has a measurable market effect. Its worth noting that in early September 2015, when it appeared our election would not result in a change in government the TSX was at 15,569. As it became clear that the government would be replaced by a less business friendly government, the performance slid. This is, of course, temporary, but from an investment perspective, the TSX has only had a 4.5% increase in value over the period from September 2015 until today, or slightly more than 1.5% per year, which is terrible growth.

Thanks for the analysis. It’s interesting to see how the different countries compare.

The only thing I would have added in the conversation would be taking a look at the expense ratio of the funds available. I know my fund choices are HORRIBLE in my 401k

Good point, Evan. I touched on it in #4 of my initial thoughts, but I certainly could have been more specific. That sucks that your choices aren’t very good at all.