Some of you probably care immensely about dividends. Some of you probably don’t even know what dividends are (except for free money in Monopoly). And some of you are probably like me: you know the basics and the concepts, but could stand to learn a bunch more to really take advantage of them.

Some of you probably care immensely about dividends. Some of you probably don’t even know what dividends are (except for free money in Monopoly). And some of you are probably like me: you know the basics and the concepts, but could stand to learn a bunch more to really take advantage of them.

Well, a few years ago I did a simple analysis where I looked into some dividend funds, and whether their dividends held up through market lows. I was surprised by what I saw. Last week, I made a comment to that effect on Millennial-Revolution.com. Another reader replied and asked if I would be willing to share my analysis.

So today’s post is that analysis. More specifically, I actually went back and redid the analysis with more up-to-date data for more funds over more years. If you would like to download the entire spreadsheet for free, sign up for the mailing list and then head on over to the Downloads page. Or just keeping scrolling (and maybe reading, too?) for the highlights.

Coles Notes Version: Dividends are never guaranteed. Even solid dividend funds can see their distributions drop by up to 20% or 30% in a given year, although overall trends should be upwards.

A Short Primer on Dividends

Before we get going, here’s a short primer for those who are clueless about dividends (but are still reading because they want to learn!)

When you buy shares in a company (also known as “stocks”), or when you buy a “fund” such as a mutual fund or exchange traded fund (ETF) that in turn owns shares in several companies, you literally own a piece of that company. That gives you the privilege to participate in any growth and profits (or losses!) that that company experiences.

If the company makes money, it really has two choices: It can reinvest in itself, such as buying better equipment, expanding into new markets, or developing new products. Or, it can distribute its profit to the people who own its stock (“shareholders”). Or some combination of both.

This distribution is called a dividend.

So, when we are talking about receiving dividends, we are literally talking about receiving some of the profit that a company has made over a given period of time.

The Connection

And that ties in directly with the topic of the day: When a company that normally pays dividends is doing poorly and not making much money, what does it do? Some will continue to pay the dividends. Some will cut them a little bit, or even cut them a lot. These are complex decisions that are well beyond the today’s post, but they impact the money that you get from your investments.

As someone approaches retirement (whether that’s earlier retirement or not), they usually adjust their investments towards paying income, which typically includes some form of dividend investing. This often takes the form of buying dividend funds. A great example of this is the “Yield Shield” that is discussed on Millennial-Revolution.com.

The problem with relying heavily on dividends for income, though, is: What happens when the companies stop making as much money? And can this be predicted in advance?

Without Further Ado…

Just before we get to my analysis, please keep in mind that I am not a financial planner and this most certainly does not constitute financial investment advice. I have collected this information and present it to you as simply another perspective to consider as you do your own research and consult your own professional advisor for your own portfolio. In other words, use this as a starting point only, and don’t rely on it. And of course, remember that past performance is no guarantee of future performance!

Ok, so I considered the following five dividend funds from Blackrock:

- CDZ – iShares S&P/TSX Canadian Dividend Aristocrats Index ETF (Canadian)

- XDV – iShares Canadian Select Dividend Index ETF (Canadian)

- CYH – iShares Global Monthly Dividend Index ETF (CAD-Hedged) (Global)

- DVY – iShares Select Dividend ETF (US)

- HDV – iShares Core High Dividend ETF (US)

I selected these because they give a nice broad perspective on different markets. If you don’t like my choices, that’s fine. It’s not rocket science. Just follow my steps and repeat the analysis with your own choice of funds. You can even use my spreadsheet if you like. Note that I personally own shares of CDZ and XDV at the time of writing.

The first step was to gather all of the data on these funds from the fund sheets at Blackrock (linked in the list above), as of last week. You’ll notice that some years are missing data, but that’s because either the fund didn’t exist at the time, or Blackrock has not yet published the data.

Then I dropped the data into a spreadsheet, formatted it, and created the charts below.

The Simple Analysis

By using total distribution by share, I’m assuming you own a fixed number of shares with the expectation of receiving regular dividends. Don’t be fooled by the fact that some funds return more than others per share; each fund has a difference share price, and therefore a different yield (distributions / price X 100%). This just means that you might own more or less of different funds.

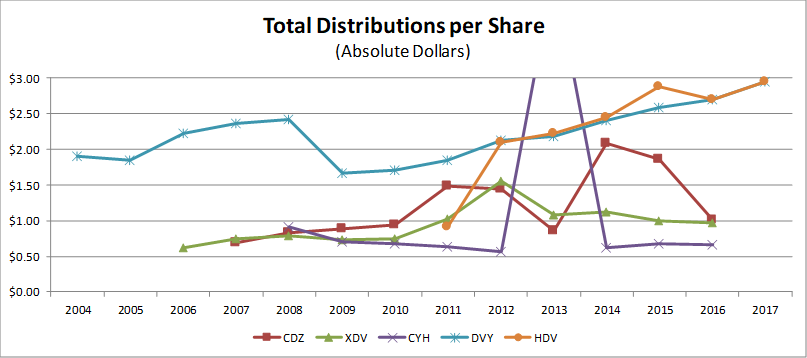

So here’s the first graph:

The first and most obvious observation is that the lines jump all over the place and are not steady, although they do seem to be trending upwards. This means at first glance that you probably should not rely purely on dividends for a substantial part of your income in a given year, unless you have a large cash cushion and can weather a decrease.

For example, look at DVY. If you purchased a bunch of shares in 2006 to 2008, you would have had to wait about 6 years for the dividends to climb back to their previous value before that 31% drop in 2009.

Conversely, my initial analysis looked at CDZ through those same years and saw that they constantly increased dividends, even as we went through a major recession and stock mark crash. But after adding more years into the analysis, look at 2013 and 2016: CDZ crashed back down. So what gives?

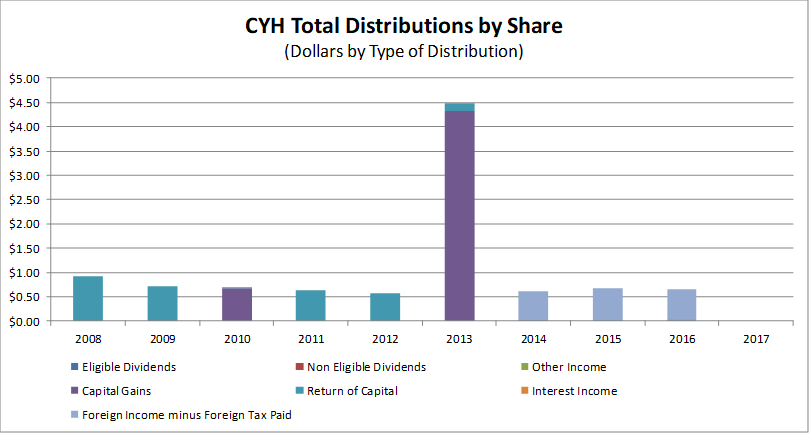

And what’s that massive distribution from CYH in 2014? It’s literally off the chart!

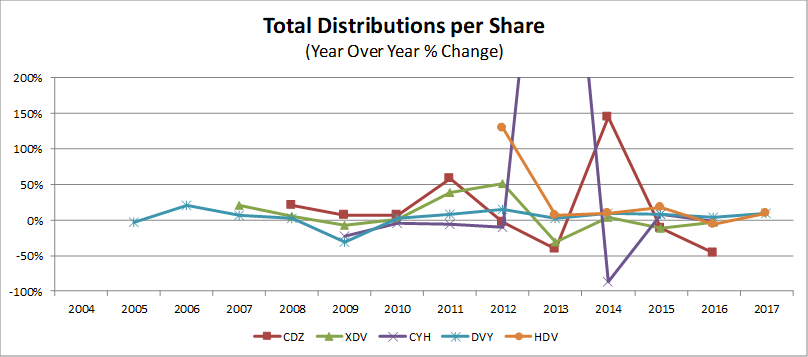

If we twist that graph a bit, look at the year over year change in distributions:

This tells a similar story as the first graph, but from a different perspective. Ideally, here you would want to see values consistently floating above 0%. But the reality is that each fund takes its turn above and below zero.

The short answer, of course, is that the individual companies are making more or less money in any given year and are adjusting their dividends accordingly. Also, some of the funds are probably adding and removing specific companies from their groups. This could result in bouncing dividends.

A Little Deeper Now

You may have noticed that I started talking about dividends and then moved on to talking about “distributions”. There’s a reason for that.

When a dividend fund pays out the dividends of the companies in the fund, it sometimes also pays you money from other sources. These collectively are known as the “total distributions”. Total distributions can include capital gains (selling some shares for more than they were purchased for), return of capital (giving you your own money back), interest, etc.

In other words, distributions from dividend funds can include more than just dividends.

Does that matter? Maybe, maybe not. It could have an impact at tax time when you have some non-dividend income to declare.

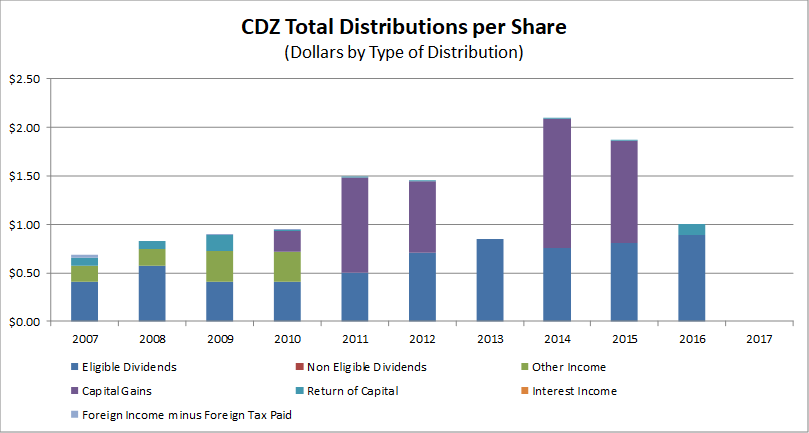

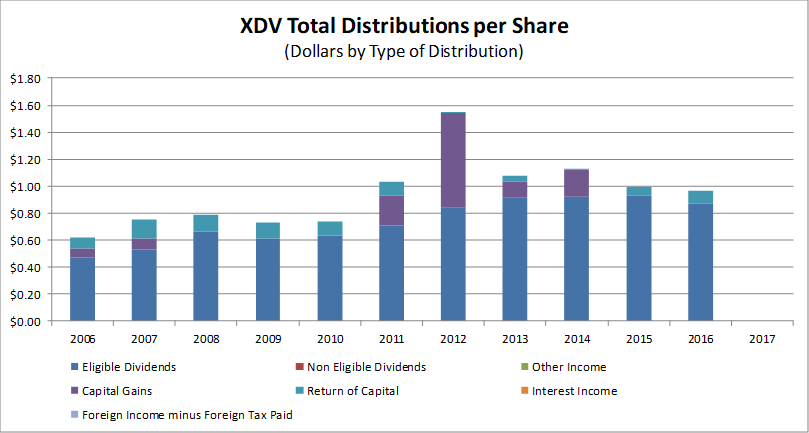

Here’s an example from CDZ, followed by XDV and CYH. (DVY and HDV sources didn’t have the data split up for me to share in this format.)

You can see that typically the dividends themselves make up at least half of the total distributions. You can also see that the increased distributions in 2011, 2012, 2014 and 2015 are due to capital gains, not dividends. That’s also what happened to CYH: They had a massive capital gain in 2013.

The Bottom Line

As with any funds or investments, things change with time. Be sure to look at trends, but also know what your risk tolerance and time horizon are. If your income or portfolio were to drop substantially, could you handle it? How can you build a portfolio that is more likely to withstand shocks? For continued reading on the topic, I recommend checking out Canadian Couch Potato. If there’s interest, I can even post about my own perspective on “Couch Potato Investing.”

Your Turn Now!

Your Turn Now!

Your Turn Now!

Your Turn Now!What do you think about dividends or dividend funds in general? Do you invest specifically in dividend-paying stocks and/or funds? Don’t forget to sign up and download the spreadsheet if you like what you see! Did you find any flaws in my analysis that I should update? Would you like to see more similar analyses?

Your Turn Now! What's On Your Mind?