The following is an approximate transcript of the talk I gave at the London ON FIRE meetup in London, Ontario on Oct 30, 2018: You Can Retire Sooner Than You Think.

The following is an approximate transcript of the talk I gave at the London ON FIRE meetup in London, Ontario on Oct 30, 2018: You Can Retire Sooner Than You Think.

1. Good evening everybody. It’s great to see so many of you out here tonight. My name is Chris Urbaniak, and I’ve been part of London ON FIRE for almost two years now, and I’m honoured to have been asked to speak tonight on the topic of early retirement.

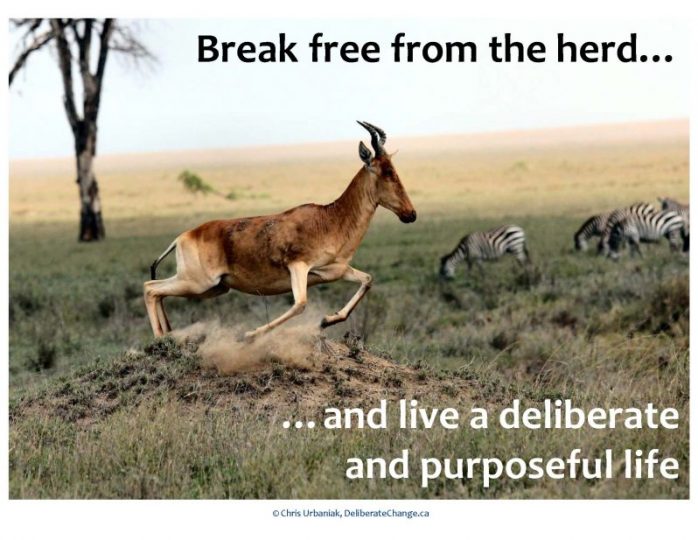

2. I wanted to start off on the right foot, so to speak. This quote (“Break Free from the herd and live a deliberate and purposeful life”) is the main mantra and underlying message of my blog DeliberateChange.ca, and is also how I’m trying to live my own life. Which ties in nicely with tonight’s conversation.

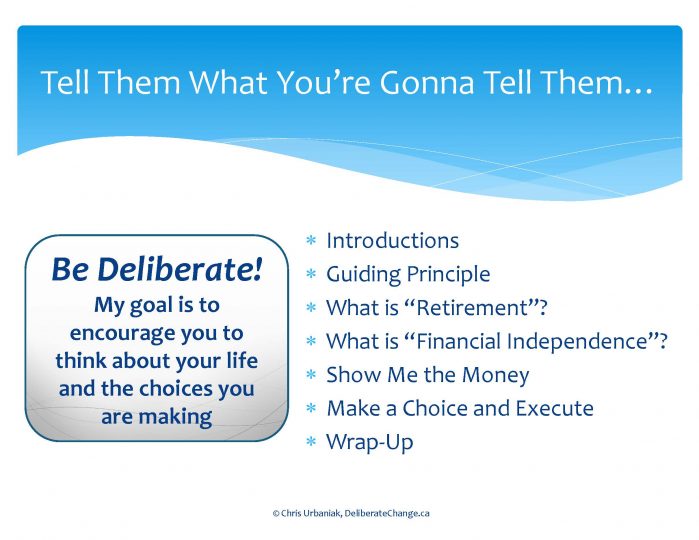

3. My goal tonight is to encourage you to think about your life and the choices you are making. I want each of us to be deliberate and purposeful with our life paths, and not necessarily do what society expects. First, we’ll get to know each other a little bit. I’ll walk through my guiding principle as well as my definitions of retirement and financial independence. We’ll then move into some examples and tactics, before wrapping up.

4. Introductions

5. So, a little about who I am not. I do not have a multi-million-dollar investment portfolio. Nor do I own any investment real estate. In fact, that’s Jeff Wybo’s sign on the front lawn of the rental property we sold last year. And nor am I a financial professional. So I guess technically, all of this is for entertainment purposes only, and do your own research on any and all decisions you make!

6. Carrying on, these are some aspects of my life that are important to me.

- Overall, I’m just a normal guy, or at least I like to think I am. I have a wonderful family.

- I’m a professional engineer who loves Excel and balancing the numbers.

- I’m good with money and am generally pretty frugal.

- As I mentioned, I blog at DeliberateChange.ca. In fact, later this week I’ll post a transcript of tonight’s talk, with all of the links and references.

- I’ve been attending Forest City Community Church for well over a decade. It’s really a church for people who would not otherwise not go to church, which is why I love it there.

- I do lots of volunteer work with my church and my community because I believe in being a net contributor vs. a net consumer. One recent example is the non-profit Forest Edge Community Pool that I lead.

7. If I could wrap up my personality in a nutshell, though, it would be family-focused, optimistic leadership, and constant learning. Just ask these people!

8. …or maybe these people…?

9. But now, the question is, “Who are you?” (This is when I went around the room and named everybody except Kyle, whose name I forgot, and Devon, who I called Dylan.) Seriously, though, this is an important question because it connects directly with the ability to discern what a deliberate and purposeful life looks like to you.

10. Guiding Principle

11. I picked this up from the famous Mr. Money Mustache: No Complainy pants allowed! If you don’t like something, then change it! We live in a time where the world is at our fingertips (sometimes quite literally), and the opportunities are boundless. You have the ability to chart out what you want: City, career, housing, spending, friends, environmental impact. So go make it happen. Without excuses.

12. Just remember as you make your choice: If you say yes to one thing, you are always saying no to something else. You can’t do it all.

13. Let’s move into some definitions now. Starting with the definition of retirement.

14. Who cares! Seriously…

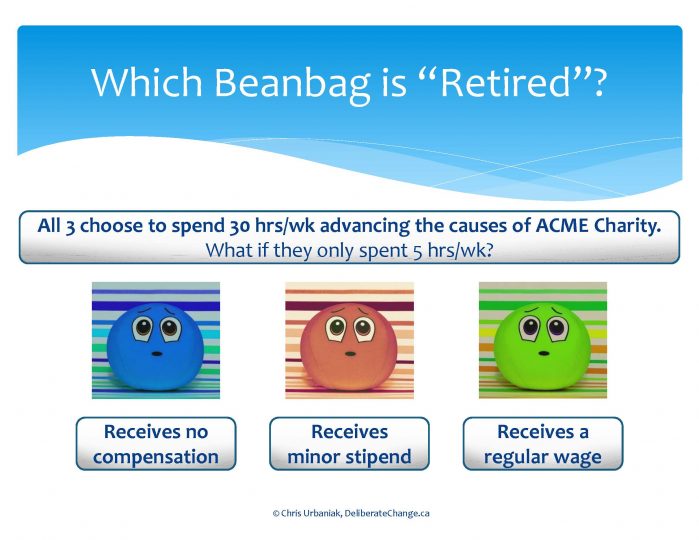

15. Let’s look at a silly example. Assume there are three beanbags, all of whom choose to spend their weeks with ACME Charity. They have no other active employment. The blue beanbag receives no compensation from ACME, whereas the green beanbag receives a regular wage. One could easily draw the conclusion that Mr. Green is working for the charity and Mr. Blue is volunteering. Therefore Mr. Green is not retired, whereas Mr. Blue is retired.

But along comes Mr. Red, who receives some minor stipend from ACME. Is he retired? Does it depend on the size of the stipend, or the strings attached? What if Mr. Blue gets paid a little bit? Is he then no longer retired? What if Mr. Green only gets paid for some of his hours? At what point do you cross from being retired to being not retired, or from being not retired to being retired? And how does this entire discussion change if they each only put in 5 hours per week instead of 30? I bet there are as many answers as there are people in the room.

16. So here’s the bottom line: Call yourself whatever you want, just don’t mislead people. Here are some links to the manifestos of some famous folks you might recognize. I’ll post them on my blog this week, so you can go check them out then.

- Mr. Money Mustache: http://www.mrmoneymustache.com/2013/02/13/mr-money-mustache-vs-the-internet-retirement-police/

- Retire by 40: http://retireby40.org/engineer-perspective-on-early-retirement/

- Our Next Life: https://ournextlife.com/2018/03/21/fire-blogger-manifesto/

- Matt McKeever: https://www.youtube.com/watch?v=SKHCfOy-oq4

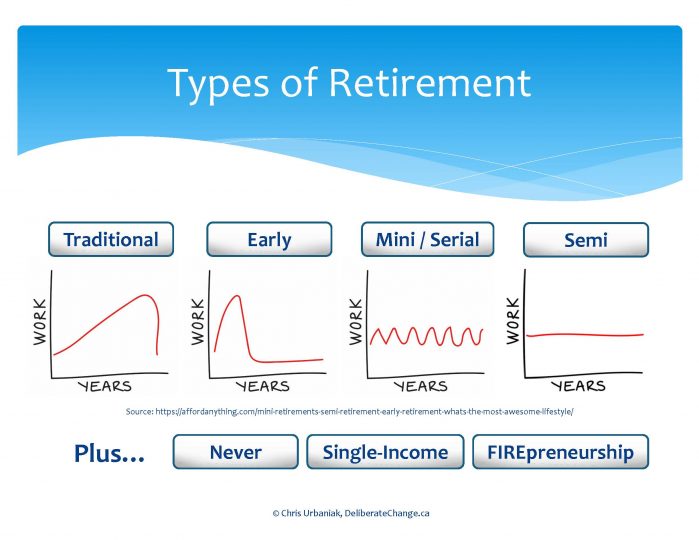

17. Part of the reason for the inconsistent definitions is because there are actually many different types of retirement, and the lines between them can be blurry. Paula Pant from AffordAnything.com suggests some of these:

- You have the traditional retirement that many baby boomers follow.

- Then there’s a full-stop early retirement.

- There’s also serial or mini retirement. My sister did this for years. Many people in this very group are doing this sort of thing. Work for a while. Take a sabbatical. Go work again. Repeat. Or semi-retirement, where you might be consistently working part-time.

- Additionally, you have people who never retire either out of financial need or because they love what they do so much (like my mechanic).

- There’s the now-famous FIREpreneurship method also common in our group here, where you basic needs are met, and you quit your regular job to go pursues a money-making passion project.

- Or you could even consider single-income households as being a form of retirement for the stay-at-home parent.

The point is to step away from the black and white retirement definition and figure out what works for you.

18. For example, Paula Pant makes the case that you can go out and enjoy mini-retirements right now. You’ll just have to return to work at some point to top up, depending on your level of financial independence. Which brings us nicely to our next definition…

19. What is “Financial Independence”?

20. Again, who cares!

21. Why? Like retirement, there are many definitions of FI. For example, when young adults grow up and can support themselves, that’s often referred to as being financially independent. I recently led a team that settled several refugees in London. Being self-supporting is their core definition of being FI.

Of course, the FIRE community in general would disagree, and rely more on the idea that being FI means you never need to work for money again. But what it really all boils down to is choice. Being FI, whatever your definition, means having choices.

22. The key is how you use those choices. You can agitate for others, like this guy on the right who stood up for precarious temp workers. You can start a new business or partnership. Go back to school and change careers. Follow your passions (many FIRE’ees become authors). As Mr. Money Mustache so correctly points out, increased financial independence leads to increased confidence to make those choices.

23. Let’s talk money for a moment now.

24. I love this quote: “Consumerism is using money you don’t have to impress people you don’t know with things you don’t need.”

25. It’s your choice. Remember the guiding principle of not complaining about your situation or circumstance. Don’t succumb society’s tug-of-war to keep up with the Joneses. But also remember, there’s nothing wrong with luxuries; just be deliberate about it.

When I was in high school, I promised myself that I would own a Ferrari 328 before I turned 40. At the time, these cars were about the same price as a mid-level BMW or Mercedes; that is, quite within reach if you want it to be. But as I’ve grown, what matters to me has changed. I still love that Ferrari, but I no longer have the desire to own one.

One of my favourite, frustrating examples is a friend of mine who complained incessantly about the high cost of daycare and how she and her husband both had to work just to get by. I’m pretty sure that combined they were making somewhere around $80k per year, which is quite reasonable. But they had car loans. And mortgage payments. And nice clothes. Don’t forget the many weekends on the town. Do you think that they considered their choices when complaining about having to work so much just to make ends meet?

Or this great example: This guy decides to start a non-profit and run across the country to raise funds and awareness about absolutely horrendous water quality situation faced by many First Nation’s. What a great thing to do!

Last minute update: Just this afternoon I had a conversation with a friend in his 50s who told me that his investments now cover all of his living expenses. Wow! What an accomplishment! So I looked him straight in the eye and asked: “Now that you can do anything you want, do you want to go to your office each and every workday?” After a long and thoughtful pause, he shared probably the most honest answer one could expect: “I don’t know.” But you can bet that he went home that night and started to think about it! And that is exactly my goal here.

26. So I hinted at this in the daycare example, but I want to be crystal clear: There are many drains on our cash flow, and we need to be particular about which ones we want to keep or cut. Four big ones that I’ve seen include cars and houses. For couples, there’s also the tendency to take your double-income status for granted, and just waste the excess. And looking from an opportunity cost perspective, so many of us just sit around wasting time.

27. But I’m not going be a complainy-pants: I’m going to offer some ideas. Anybody heard of the 10% rule for cars? It’s tough! It means never buy a car that costs more outright than 10% of your annual income. So, if you make $80k/yr, don’t spend more than $8k on a car. And there are many decent $8k cars around. The 15% or 20% rule for cars is perhaps more achievable for most people, but not try for 10%? It’s definitely a simplification, because you should really consider the total cost of car ownership, but it’s a good starting point.

For housing, obviously you can house hack. “But I don’t want to live with anybody else or be a landlord.” Fair enough. Just remember that your choice. For dual-income couples, pretend only one of you works, and then live on just their income. And instead of sitting around, pick up a side hustle or some new skills.

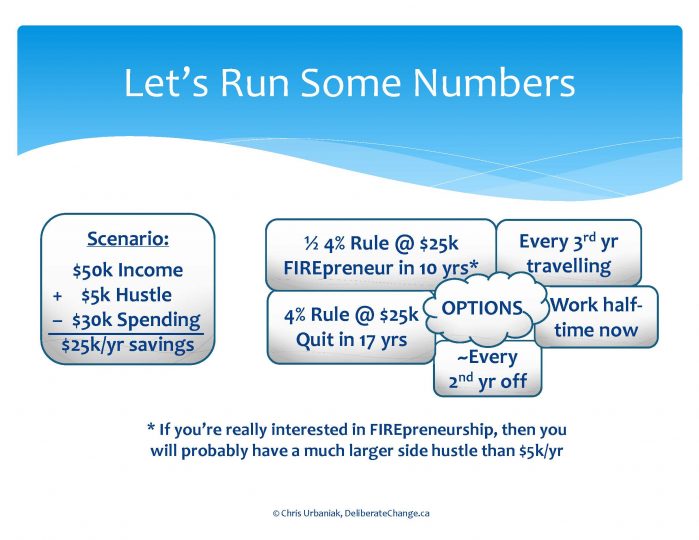

28. Now that we have an idea on how we can control some of our spending habits, and we understand different levels and types of retirement and FI, let’s run some numbers to pull it all together.

Assume you’re making $50k plus a $5k side hustle, and you spend $30k. These are very achievable numbers for most people, if you want it badly enough. (Don’t worry about over-complicating the scenario with taxes, etc.; it’s just an illustration.) Now, with these healthy earning and spending patterns, you open up an entire world of choices.

- You’re half-way to achieving the 4% rule in 10 years, which will allow you to take the plunge into FIREpreneurship. (Although if you’re entrepreneurial enough to do this, your side hustle is probably larger than $5k.)

- Or just wait 17 years and quit full stop.

- Or just start working half-time now.

- You could choose to work only every other year, or travel extensively every third year.

The point is that you have options because you have healthy spending and earning habits.

29. But how on earth do you make those choices and follow through?

30. First, check your ego at the door. Who cares if you call yourself retired? Who cares if you call yourself financially independent?

31. Remember Rafiki? Who are you, and what do you want your collage to look like? What is your why? What are you passionate about? Have you thought about what motivates you, and what makes you so angry that you have to fight to change it?

32. As you work through those questions, hopefully you’ll start to gain a little clarity. You’ll start to see the difference between Here and There. And then you can start moving in that direction.

You’re not trying to land a rocket on Mars, so you don’t need to know all of the little tiny details upfront. You can start with small steps in the right direction and work out the details along the journey.

Take this owl for instance. When she flies from here to there, does she create a detailed itinerary and flight plan? Or does she see something enticing and head over? I’m no biologist or birder, but the answer is probably something in the middle. She knows what she wants, and she course corrects as she goes along depending on what she encounters.

33. But what if you screw up? I curled competitively back in high school. My dad, the coach, taught me several lessons that are as applicable in life as they are on the ice. Consequence of Error is one of them. It’s really a risk management strategy that says sometimes the “wrong shot” made is better than the “right shot” missed, particularly if the “right shot” has a high probably of failure.

So what is your definition of FIRE failure? It could be as simple as having to go back to work. Well, if you work longer now, are you not simply guaranteeing failure? Of course, you have to consider all sorts of things such as the type, quality and availability of work now vs. at some future point. This failure would likely be easier to handle in your 40s than in your 70s! But in many cases, does it really matter if you “fail” at FIRE? As Matt McKeever says, “You can always pull the parachute on the way down”.

34. Alright, let’s wrap this up.

35. In most situations, the grass is not greener on the other side. It’s greener where you water it. Be sure to remember that as you’re planning your next moves. You might actually be better offer choosing to be content and experience joy in your current situation, or you might still wish to change it up.

36. Which brings me back to the main point: will you follow the guiding principle of not complaining, but taking action instead? Will you check your ego at the door? And will you make a choice and execute?

37. Because you can retire sooner than you think by choosing to live your deliberate and purposeful life.

38. Thank you.

Great talk last night Chris. Keep up the great work!

Thanks Angeline! It was great to meet you; thanks for coming out 🙂

It’s really a nice and useful

piece of information. I’m satisfied

that you just shared this helpful information with us.

Please stay us informed like this. Thank you for

sharing.